4 Reasons Why You Should (Possibly) Not Delay Filing Bankruptcy

Click Here For Your Free Bankruptcy Evaluation

In A Nutshell

(1) Stress (Collection Efforts)

(2) Wage Garnishment

(3) Cost Of Bankruptcy (Attorney Fee Could Be More If You Delay)

(4) Larger Chapter 13 Payment

In More Detail

(1) Stress (Collection Efforts)

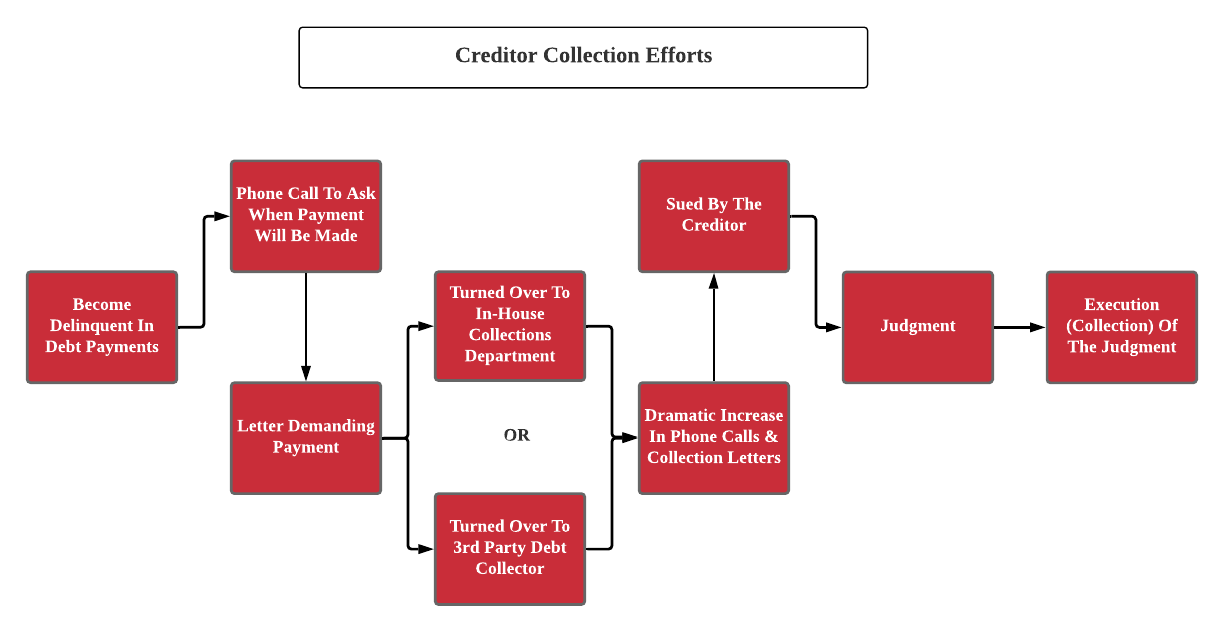

Collection efforts by creditors can take on many forms and will progress as you become more delinquent on your debt.

UNSECURED DEBTS (i.e. credit cards, medical bills). When you miss a monthly payment on an unsecured debt the creditor will typically call you to determine the reason for your delinquency. The creditor will continue to call until they get some resolution. Many creditors will then send you a letter in the mail requesting payment and threatening further action if the debt is not paid. As the debt falls further and behind, the creditor will turn the debt over to their in-house debt collection department or a third party company that specializes in debt collection. This is the dreaded period where the collection phone calls you receive increase dramatically. The conversations you will have with the debt collector (should you choose to answer the calls) will be of a threatening nature.

Next, the collection effort will be turned over to an attorney who will bring a lawsuit against you. Because you owe the debt and will not be able to fight the veracity of the allegations in the lawsuit, you will then have a judgment against you. The creditor will seek to execute the judgment against you meaning they will try to get out of you what is owed. In North Carolina, the sheriff will be the party that will attempt to execute this judgment on behalf of the creditor. Through this process you could lose a portion of the property you own.

SECURED DEBTS (i.e. mortgage on home, vehicle loan). When you miss a payment on a secured debt the collection effort of the creditor will likely begin in the same manner as the collection of an unsecured debt. You will receive phone calls inquiring about your delinquency and possibly a letter. But the most consequential effort a secured creditor can take is to take back the collateral used to secure the debt. This can be done through foreclosure of your home or repossession of your vehicle.

I often get asked, “How long do I have before the creditor will foreclose/repossess?” This answer often depends on your situation and the creditor. Some creditors act faster than others. Foreclosure is a somewhat lengthy process that a creditor has to go through to get the house from you. There are hearing dates, a sale date, and a 10 day upset period before you are actually forced to get out of the house. Repossession of your vehicle can occur (potentially) following one missed payment.

BANKRUPTCY WILL STOP ALL COLLECTION EFFORTS. As soon as your bankruptcy is filed, you get the benefit of the imposition of the Automatic Stay. The Automatic Stay stops all collection efforts immediately. No more phone calls, letters, lawsuits, or execution of judgments. If you are facing foreclosure or repossession, then bankruptcy will stop these collection efforts as well. Through your bankruptcy (Chapter 13 for this situation) you will be able to cure your default and keep the collateral used to secure the debt if you desire.

(2) Wage Garnishment

Another type of collection effort that often causes great headache for individuals is wage garnishment. A creditor that has a judgment against an individual can sometimes collect upon that judgment by having the individual’s wages garnishment. Practically this means that the individual’s employer has to send a certain amount to the creditor from each of the individual’s paychecks. The individual never actually sees this money come to them. The IRS can also garnish one’s wages for taxes owed.

Obviously wage garnishment can have major consequences for an individual and his family. It causes the take home income of an individual to be severely reduced with almost no warning. This often results in other bills owed by the individual going unpaid.

For example: you make $1,000 per week from your employer. Typically, after taxes and insurance are deducted from your income, you bring home $750. Then a creditor begins to garnish your wages and requires the employer to send them $250 per paycheck. Now you take home $500.

BANKRUPTCY STOPS WAGE GARNISHMENT. As mentioned above, bankruptcy stops all collection efforts. This includes wage garnishment from judgment creditors and the IRS. Bankruptcy allows you to deal with the creditors by a means other than wage garnishment. Shortly following the bankruptcy you will begin to receive your full paycheck again ($750 from the example above). Any wages garnished following the bankruptcy filing will be returned to you.

(3) Cost Of Bankruptcy (Attorney Fee Could Be More If You Delay)

It is certainly not always the case that delaying your bankruptcy will cause a higher attorney fee. In fact, sometimes delaying can be used as a strategic bankruptcy planning tool. On the other hand, sometimes a delay can cause your situation to become more complex resulting in more work for an attorney resulting in a higher attorney fee.

For example: prior to your unsecured debt turning into a judgment your bankruptcy petition will be “run-of-the-mill.” Meaning the attorney will simply list the creditor in your petition and your unsecured debt will be discharged. A delay in your bankruptcy filing could result in the unsecured debt turning into a judgment against you. In North Carolina a judgment solely against you in a county where you own real estate (not owned jointly with a spouse) attaches to that property. When filing a bankruptcy for you with this type of judgment, the attorney has to file an extra motion to remove (or “avoid”) the judgment from the property. Because of this extra motion being filed, many attorneys will charge an additional fee.

(4) Larger Chapter 13 Payment

Your Chapter 13 bankruptcy payment is based upon many factors. Sometimes delaying your bankruptcy filing can cause your bankruptcy payment to be higher than it would have been had you filed sooner. If you think it is a possibility that you may file bankruptcy now or in the near future, then you should complete our online intake form to provide me with the information I need to examine your situation for free. 2 examples below:

EXAMPLE 1: you are behind on your mortgage (the amount you are behind is called your “arrears”). Through your Chapter 13 payment, you will pay your mortgage’s normal monthly payment as well as the arrearage you owe.

Let’s assume your monthly mortgage payment is $500 and in January you are $3,000 behind on your mortgage. If you file a Chapter 13 bankruptcy in January then your monthly bankruptcy payment will include $500 plus $50 ($3000 / 60 months) for a total of $550 going toward your mortgage.

If you delay and file a Chapter 13 bankruptcy in July, then you will now be $6,000 behind on your mortgage. Your monthly bankruptcy payment will include $500 plus $100 ($6,000 / 60) for a total of $600 going toward your mortgage.

EXAMPLE 2: Let’s assume that you are required to pay back 100% of your unsecured debt through your Chapter 13 bankruptcy payment (this is somewhat rare but certainly happens in some cases). If you are not making any monthly payments towards these debts, then the more you delay the more the debts increase. The more you owe at the time of your bankruptcy filing the higher your monthly payment will be.